Thought Leadership

New MIT Business Travel Dashboard Debuts in DataPool

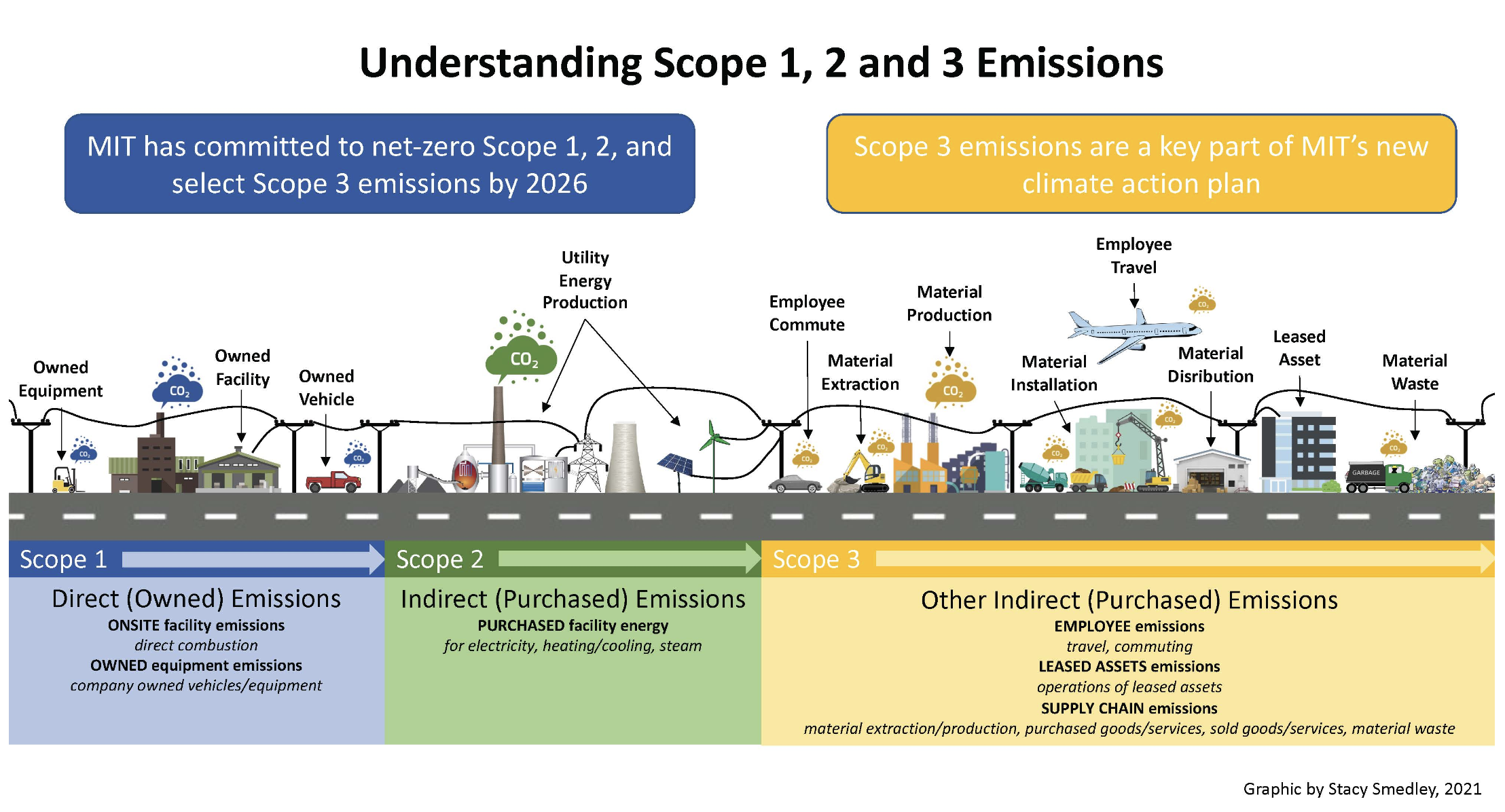

Fast Forward: MIT’s Climate Action Plan for the Decade, requires MIT to evaluate and expand its greenhouse gas portfolio accounting to include relevant Scope 3 emissions (e.g., purchased goods and services, sponsored MIT travel, commuting) by 2023. The newly launched MIT Business Travel - Scope 3 Emissions Dashboard is a climate action planning tool that can enable users to understand the scale of MIT's Scope 3 footprint and identify opportunities for reduction. The dashboard includes a visualization comparing Scope 3 with Scope 1 and 2 emissions, as well as visualizations specific to MIT-sponsored travel or business travel including travel emissions versus expense, travel emissions by year, and travel emissions attributed to school area. This dashboard is the first in a series of anticipated Scope 3 visualizations that allow users to understand the scale of MIT's Scope 3 footprint and opportunities for reduction.

Visit the Dashboard or learn more about Scope definitions and categories below.

Scope Definitions

1: Direct emissions from operations that are owned or controlled by MIT (e.g., burning of natural gas at MIT’s cogeneration plant or use of MIT-owned vehicles)

2: Indirect emissions from the generation of purchased or acquired electricity, steam, heating, or cooling consumed by MIT

3: All other indirect emissions that occur in the value chain of MIT, including both upstream and downstream emissions

The following Scope 3 categories are relevant to MIT:

3.1. Purchased Goods and Services: Extraction, production, and transportation of goods and services purchased by MIT. NOTE: this is an incomplete estimate based on a fraction of MIT’s purchased goods from FY16. It does on include all purchased goods or any services. As such, it should be viewed as a significant underestimate of the GHG emissions due to MIT’s purchased goods and services. Efforts are underway to capture a more complete estimate of this category.

3.2. Capital Goods: Extraction, production, and transportation of capital goods purchased or acquired by MIT. Capital goods include equipment and buildings. NOTE: this is an incomplete estimate that only includes emissions associated with building construction and renovation. Efforts are underway to capture emissions from equipment.

3.3. Fuel and Energy: Upstream emissions associated with extraction, production, and transportation of fuels and electricity purchased or acquired by MIT, not already accounted for in Scope 1 or Scope 2 emissions, which include direct emissions from burning fossil fuels.

3.5 Waste: Disposal and treatment of waste generated in MIT’s operations by facilities that are not owned or controlled by MIT. Recycling is calculated as a net value of the burdens due to recycling and the benefits of avoided emissions from producing virgin materials. The net value is negative (a net benefit), which is why the GHG emission of treating MIT’s waste has a negative value (the recycling benefits are larger than the burdens of waste treatment).

3.6 Business Travel: Emissions from transportation (air, road, rail), accommodations, and food for MIT employees on MIT-sponsored business travel.

3.7 Employee Commuting: Transportation of MIT community members between their residences and their worksites.

3.8 Upstream Leased Assets: Operation of assets leased by MIT. This includes the energy consumption of buildings that MIT leases for the MIT community to use.

3.13 Downstream Leased Assets: Operation of assets owned by MIT and leased to other entities. This includes energy consumption of buildings that MIT owns and leases to others.